This article is brought to you by our sponsor, Empower. Empower Personal Wealth, LLC (“EPW”) compensates Well Kept Wallet for new leads. Well Kept Wallet is not an investment client of Personal Capital Advisors Corporation or Empower Advisory Group, LLC.

Knowing if you’re saving enough for retirement is a question worth asking repeatedly during your career. Checking your current progress with a retirement planner is one of the most effective ways to compare several scenarios to save confidently.

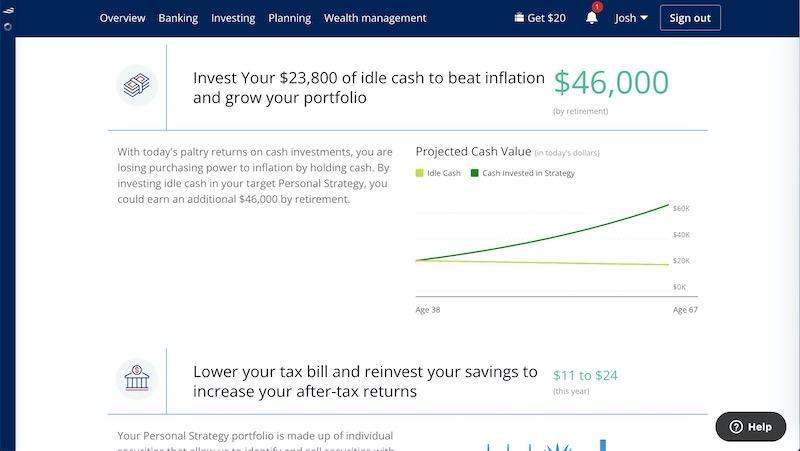

Personalized Retirement Projections

General retirement savings tips, such as investing 10% of your income in retirement accounts or saving 25 times your annual expenses, are excellent starting points. However, you lack a personalized plan with a blanket approach that can make you wonder if you’re on the right track.

A few years into my career, I became frustrated with following only the basic advice once I had a firm grasp on my immediate expenses and could focus more intently on long-term goals. Older colleagues encouraging me to get serious about retirement in my 20s was an additional factor.

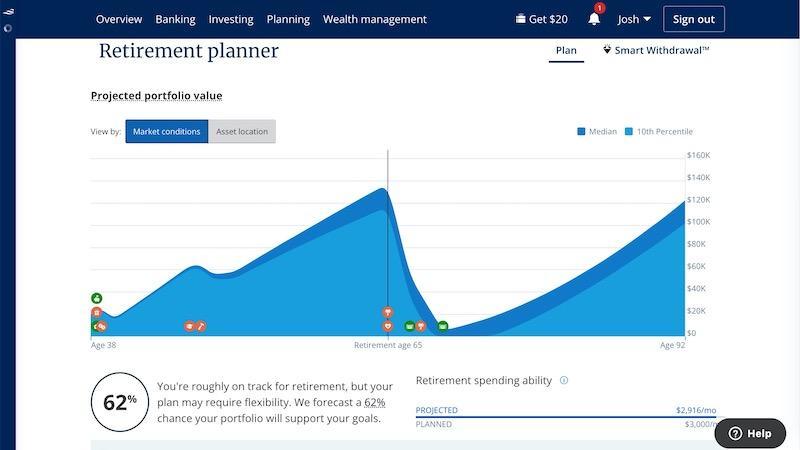

Empower offers a free retirement planner that I regularly use to monitor my finances. You can enter multiple pre- and post-retirement goals and adjust your retirement age to visualize your progress.

Consider running the following calculations through the planner:

- Income and expenses: Run situations with different income and expense amounts.

- Goals: See how much you need to save for upcoming goals and lifestyle changes.

- Life events: Add notable moments such as children, weddings, and college.

- Retirement age: Explore early, on-time, and delayed target retirement dates.

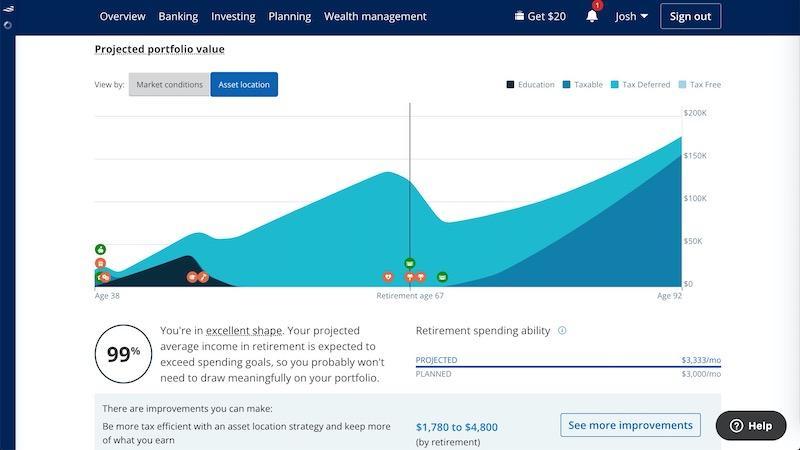

The calculator runs 5,000 Monte Carlo simulations to project your retirement savings, Social Security income, and investment asset allocation. You can also include the Dot Com or Great Recession market drawdown patterns in your simulations to predicate your portfolio performance.

You will see a probability of retirement success, your retirement spending ability, and suggested improvements.

Be sure to include all your financial accounts and income streams for an accurate projection. For instance, be sure to list pension and rental property income. You can also add one-time windfalls, such as a home sale or inheritance.

Further, I like that the planner makes state-specific tax calculations and allows you to edit your income tax bracket and inflation rate assumptions. A no-frills retirement calculator is less likely to offer these details.

Track Multiple Goals

A sound financial plan helps you afford near-term, mid-term, and long-term goals. Life is a journey; adding these objectives lets you see the whole story upfront. As a result, you’re less likely to sacrifice milestones that are still years away or delay retirement.

Major purchases on your wishlist may include:

- Boat

- Classic car

- Investment Properties

- Hobbies

- Home renovations or upgrades

- Replacement vehicles

- Travel

- Vacation home

If you’re like me, there are several times when you ask, “Can we afford this right now?” It can be easy to focus almost exclusively on your immediate priorities and forget about retirement still decades away. Running the numbers adds confidence to your decision process.

A written plan helps allocate your income for your pre-retirement goals while continuing to save for retirement monthly. The retirement calculator’s chart also enables you to see how the acquisition impacts your saving ability and future nest egg balance.

Suppose you like digging deep into the data. In that case, you can view a cash flow table highlighting your starting portfolio value, yearly spending, and cash savings amounts during your accumulation phase and retirement years.

Plotting your current financial ambitions with the one-time or ongoing expense amount and action date displays your estimated portfolio value by age. You can use the other Empower Retirement App features to monitor your cash flow, real-time account balances, and more.

Plan for the Unexpected

Surprise bills are inevitable, and boosting your emergency fund to cover the cost is one of several tactics to pursue. Usually, you can plan ahead of time for expenses like a roof replacement or new car tires without knowing the precise date or dollar amount.

However, other situations require your best estimate. You may need to pay for the entire amount out of pocket or cover the difference that insurance doesn’t reimburse.

Using your personal circumstances and expert research as a baseline, you should also set aside funds for the following:

- Funerals

- Job loss

- Medical bills

- Pet emergencies

- Storm-related home repairs

- Tax and insurance increases

- Utility repairs and replacement

- Untimely vehicle repairs

Depending on your budgeting style, sinking funds save money for a specific purpose. Just like you have a retirement fund, these dedicated accounts prevent you from losing your savings progress for other goals.

If you have an eligible healthcare plan, a health savings account (HSA) lets you save for future medical expenses with tax-deductible contributions and tax-free withdrawals. Your employer may also offer tax-advantaged accounts that can address certain costs during your working years so you can allocate more of your take-home pay towards your net worth.

Periodically reviewing your insurance policies and deductibles can ensure that you’re adequately insured while minimizing your potential out-of-pocket expenses.

Family Planning and Education

Updating your retirement plan and monthly expenses as your household size grows and you add more dependents is also essential for accuracy. As a father of five, my spending and savings patterns have shifted over the years to set my children up for financial success.

Expenses you will want to plan for include:

- Dependent support (i.e., children and aging relatives)

- Education

- Weddings

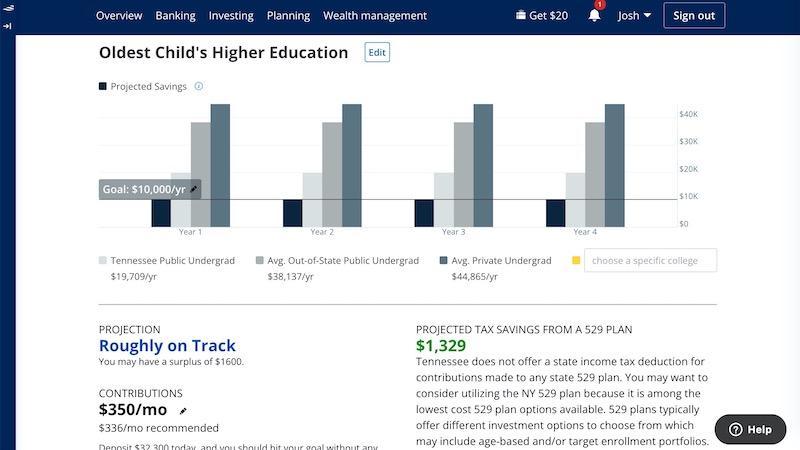

When planning for college expenses, Empower Retirement Planner displays the average annual tuition costs for in-state undergraduate, out-of-state, private universities, and an institution of your choice.

Start by entering your anticipated annual contribution amount during your child’s college education, plus how much is saved so far. These numbers estimate how much you need to save each month to reach this particular savings goal during your child’s adolescence.

This exercise helps determine if you can afford these life events and retirement. For example, I currently have to contribute less to the college fund to avoid negative cash flow in retirement.

If you’re starting your parenting journey or will be soon, running these calculations years in advance provides plenty of time to adjust and achieve a desirable retirement portfolio value.

As a side benefit, the planner also estimates your potential tax savings from 529 contributions. It looks for other ways to optimize your cash investments, too.

Make a Retirement Budget

Estimating your retirement expenses is pivotal. The lifestyle you anticipate living determines how much you need to save and how quickly you can draw down your balance.

Several changes are afoot as you stop earning a full-time income but switch to Social Security and your investments to pay the bills. You may also become eligible for Medicare at age 65 and must navigate changing healthcare premiums.

Your retirement budget should include the following:

- Core monthly expenses: Food, utilities, insurance, transportation, and housing.

- Healthcare: Pre-Medicare health coverage, Medicare supplements, etc.

- Travel: Vacations and visiting family or friends.

- Social Security: Your estimated annual benefits are based on your starting age.

- Other income: Salary from a part-time job, pensions, annuities, and investment properties.

You may need to account for a coverage gap between your retirement age and when Social Security and Medicare benefits kick in. Your projections may indicate a sizable drop in your projected portfolio balance before rebounding once your benefits start.

Run several scenarios to find a practical retirement age and income budget.

Maximize Tax-Advantaged Retirement Accounts

Traditional and Roth retirement accounts can be the foundation of life savings, so you’re not relying entirely on Social Security. Specially, your contributions are tax-advantaged as you only pay taxes once.

Workplace accounts such as 401(k), 403(b), and Thrift Savings Plan (TSP) have high annual contribution limits, and your employer may also match a certain amount. Fewer employers offer pension plans, making these contributions more valuable than before.

Individual retirement accounts (IRAs) also play a role if you want additional financial flexibility or if your current employer doesn’t offer retirement benefits. You can simultaneously contribute to IRAs and employer-sponsored plans to increase your retirement reserves.

Some of the best practices include:

- Recurring contributions: Automating your contributions to give your portfolio the most opportunity to invest new money and earn compound interest.

- Catch-up contributions: You can make additional retirement account “catch-up contributions” starting at age 55. Use this perk to capture more tax-friendly gains or to help offset a forecasted cash flow shortage.

- Diversification: A proper allocation for your age and risk tolerance helps ensure you are not too aggressive or conservative. Position sizing also manages risk to optimize your investment returns in bullish or bearish market cycles.

- Tax efficiency: Certain income-producing assets are a better fit for tax-advantaged accounts to reduce your lifetime tax burden. Further, decide if the traditional tax-deferred or Roth tax-free treatment is better for your retirement budget.

Syncing your accounts with Empower allows you to track your portfolio performance and real-time value. Routine Retirement Planner check-ins help you determine whether you’re still on track.

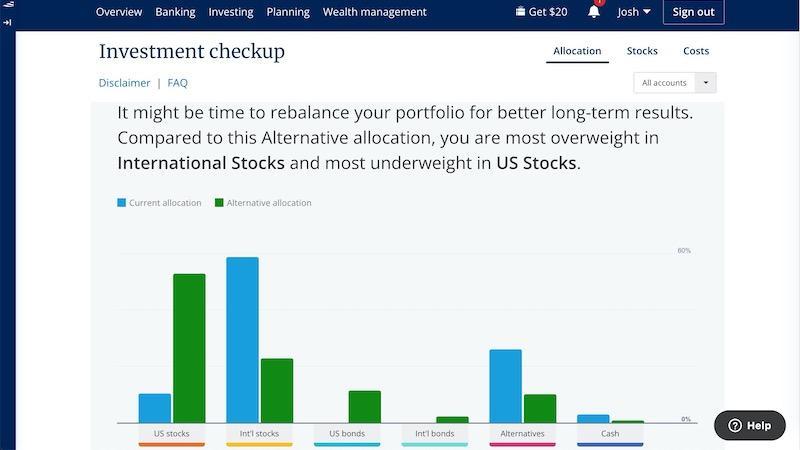

Routine Investment Checkups

Setting up your retirement portfolio is just the first step to reaching your target balance. You want to regularly review your asset allocation to ensure you remain adequately diversified for your age and risk tolerance.

Empower provides on-demand checkups highlighting your current allocations and an alternative allocation that can optimize your potential returns and reduce your portfolio risk. Thanks to its level of detail, it’s one of my favorite free portfolio analysis tools for routine rebalancing.

Specifically, you can view the historical returns and risk for your current allocation and alternative portfolios. Further, you will see which asset classes you have the most and least exposure to and should concentrate on first during your next rebalance.

You may have too much exposure to domestic stocks and may benefit from more international stock funds. While less exciting, it may be time to add more bonds to your portfolio for stability and income.

The checkup goes further by providing a precise dollar amount to increase or decrease your assets to achieve an ideal balance. Not every investing app provides similar insights, and having an extra set of eyes on your portfolio can be priceless.

Your alternative allocation percentages are based on several questions you answer in your investment profile. You can periodically re-answer this questionnaire for an accurate assessment as your career and savings habits progress.

The planner backtests your portfolio against investment returns dating back to 1992. While historical performance doesn’t foretell future results, incorporating 30 years of bullish and bearish market cycles is an excellent indicator.

Analyze Retirement Fees

Investment fees are easy to overlook and focus almost entirely on potential investment performance and portfolio diversification. However, the ongoing costs of expensive funds or high 401(k) administration fees can significantly damper your lifetime earnings.

While retirement plan providers must disclose all applicable fees, the amounts may seem trivial compared to your contribution amounts and potential growth. Additionally, many workers are simply unaware of the fee amounts and their potential implications.

Your retirement plans can include the following fees:

- Investment fees: Mutual fund and ETF expense ratios, trading commissions, etc.

- Plan fees: Administrative fees, recordkeeping expenses, etc.

- Service fees: Optional services such as loans and advisory services.

Many fees are percentage-based, so your costs increase as your portfolio balance expands. Annual plan administration fees and trading commissions are usually a fixed dollar amount.

Empower Retirement Planner estimates your lifetime fees by analyzing your current portfolio, contribution amounts, and account expenses. It also calculates annual fees by investment in your synced employer-sponsored accounts and IRAs.

Most individuals pay approximately 1% in annual 401(k) fees. This step helps you assess your current plan and identify areas for improvement.

Depending on your 401(k) investment options, you can switch from actively managed funds to low-cost index funds or target-date funds while maintaining a diversified portfolio corresponding to your goals.

If you have a lousy 401(k) plan, a common strategy is contributing enough to earn your employer’s match and invest the remainder of your retirement savings in individual accounts. Your personal IRA will likely be fee-free and have low-cost investment choices.

Make Improvements

The planner’s simulations use your starting portfolio balance and goals to suggest improvements that bolster your immediate and retirement finances. These insightful solutions help you know where to focus with specific action steps.

The changes can be easy to implement depending on your goals and finances. Running several possibilities also helps you see when you can reach financial independence.

The suggestions may help you:

- Improve your asset allocation

- Increase your retirement balance

- Reduce tax liability

If this is the first time analyzing your retirement strategy, these tips can be valuable and provide peace of mind.

Final Thoughts

The Empower Retirement Planner makes retirement planning straightforward, as you can quickly view your progress, add goals, and make corresponding changes.

You can also free-run multiple scenarios and simulations to get peace of mind.

")

")